Understanding the Reverse Charge Mechanism in GST

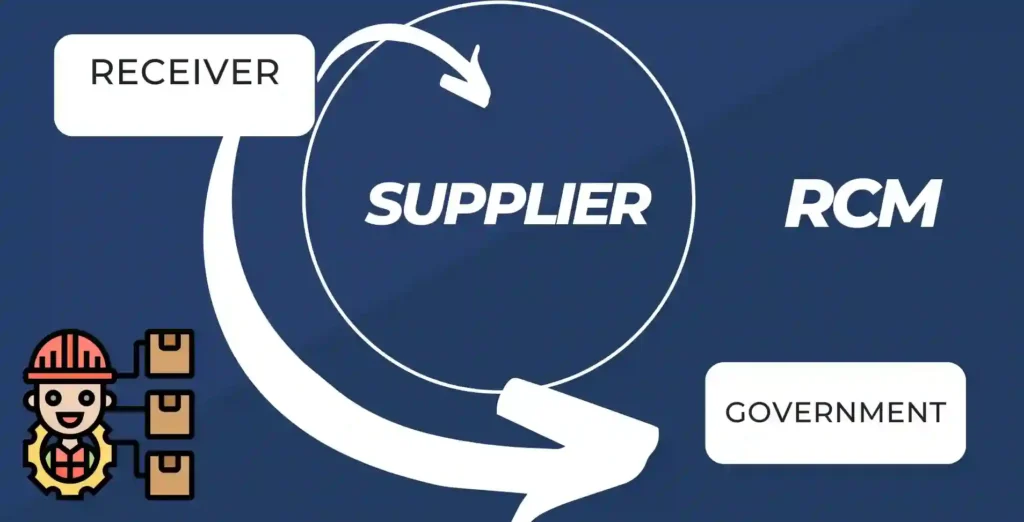

The Reverse Charge Mechanism (RCM) under India’s Goods and Services Tax (GST) framework is a critical concept that shifts the responsibility of tax payment from the supplier to the recipient of goods or services. This blog delves into the RCM in GST, its applicability, and how Sonic Software simplifies compliance for businesses.

When Does RCM Apply?

Notified Goods and Services

The GST Council notifies certain goods and services under RCM. Examples include cashew nuts, silk yarn, legal services, and certain freight services.Unregistered Suppliers

If a registered recipient procures goods or services from an unregistered supplier, the recipient must pay GST under RCM.Import of Services

When services are imported from a supplier outside India, the recipient in India is required to pay GST under RCM.E-Commerce Transactions

E-commerce operators must pay GST for certain transactions conducted through their platforms.

Key Compliance Requirements Under RCM

- Self-Invoicing: The recipient must issue a self-invoice for transactions under RCM.

- Tax Payment: GST must be paid directly to the government by the recipient.

- Input Tax Credit (ITC): The recipient can claim ITC for the tax paid under RCM, subject to eligibility.

- Detailed Record-Keeping: Maintain accurate records of RCM transactions for audit and compliance purpose

Key Features of RCM

- Tax Liability: The recipient is responsible for paying the GST to the government.

- Self-Invoicing: The recipient must generate an invoice for RCM transactions.

- Input Tax Credit (ITC): The tax paid under RCM can be claimed as ITC, subject to conditions.

- Applicability: RCM is applicable only for certain goods, services, or specified circumstances.

Challenges with RCM

- Increased Compliance Burden: Additional tasks such as self-invoicing and detailed record-keeping.

- Risk of Errors: Incorrect classification of transactions may lead to penalties.

- Cash Flow Impact: Immediate payment of GST under RCM can affect business cash flow.

| Basis | Reverse Charge | Forward Charge |

|---|---|---|

| Assessment | The recipient self-assesses the tax; the supplier does not charge GST in the invoice. | The supplier assesses the tax and transfers ITC to the recipient. |

| Payment to Government | The recipient is liable to pay GST to the government. | The supplier is liable to pay GST to the government. |

| Registration | The recipient must register under GST. | The supplier must register under GST. |

| Due Date of Payment | Monthly | Monthly |

| Mode of Payment | Payment is made via Electronic Cash Ledger. The recipient cannot use the electronic credit ledger for GST on such supply, but can claim Input Tax Credit after payment under RCM. |

Payment can be made via: • Electronic Credit Ledger • Electronic Cash Ledger |

Frequently Asked Questions (FAQ)

Reverse Charge Mechanism (RCM) is a GST system where the buyer (recipient) pays GST instead of the seller for certain notified goods and services.

Yes, If a registered business buys services from an unregistered supplier (like legal services from an advocate), the buyer must pay GST directly to the government under RCM.

Under RCM, the recipient of goods or services is responsible for paying GST, not the supplier.

RCM applies in cases such as:

- Purchase from unregistered suppliers

- Notified services (advocate, GTA, director services, etc.)

- Import of services

The software is cloud-based and works on desktop, laptop, and mobile anytime, anywhere.

GST is calculated at the applicable GST rate on the value of goods or services. The recipient pays CGST & SGST (intra-state) or IGST (inter-state).

Yes. If a transaction falls under RCM provisions, compliance is mandatory, and failure to pay GST may attract penalties.